Convolutional Neural Network – Based Algorithm for Currency Exchange Rate Prediction

Article Sidebar

Main Article Content

Abstract

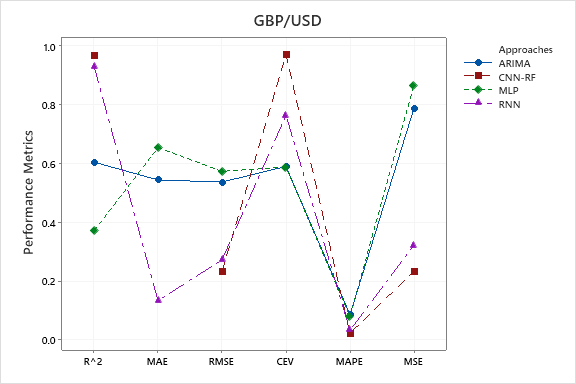

The foreign exchange market is one of the complex monetary markets in the world. Each day trillions of dollars are traded in the FOREX market by banks, retail traders, corporations, and individuals. It is very challenging to predict the price in advance due to the complex, volatile and high fluctuation. Investors and traders are constantly searching for innovative ways to outperform the market and increase their profits. As an outcome, forecasting models are continually being developed by scholars around the globe to accurately predict the characteristics of this nascent market. This study intends to apply the Random Forest (RF) approach to Convolutional Neural Networks, which involves two key steps. The first step is starting with feature selection using Convolutional neural network.The attention layer is then employed to assign weight.The random forest strategy is designed in the second stage to generate high-quality feature subsets. Thus the better result generated by CNN-RF model. Actually, this strategy combines the advantages of two different strategies to produce an outcome that is more consistent with what exchange market decision-makers anticipate happening in the exchange market.The main currency pairs considered in this study's proposed model for predicting exchange rates five and ten minutes in advance are the British Pound Sterling (GBP) against the US Dollar (USD), the Australian Dollar (AUD) against the US Dollar (USD), and the European Euro (EUR) against the Canadian Dollar (CAD) are also used to evaluate the performance of the proposed model. In compared to the other three models (Multi-Layer Perceptron, Autoregressive Integrated Moving Average, and Recurrent Neural Network), CNN-RF yields better results. This conclusion has been backed by a large body of empirical research, which also suggested that this methodology be regularly used due to its high efficacy.

Article Details

References

T.N.Pandey et al.,”A novel committee machine and reviews of neural network and statistical models for currency Exchange Rate prediction: An experimental analysis”, Journal of King Saud University–Computer and Information Sciences, vol.32, no.9,pp.987-999, 2020.

S.K. Chandra, M. Sumathi, S.N. Sivanandam, Foreign exchange rate forecasting using Levenberg-Marquardt learning algorithm, Indian J. Sci. Technol. 9 (8),1–5,2016.

K.o.Shea, R.Nash, “An Introduction to Convolutional Neural Networks”, arXiv:1511.08458v2,2015.

Y.A.,Andrade-Ambriz, ,S., Ledesma, M.A. Ibarra-Manzano, M.I.Oros-Flores, and D.L. Almanza-Ojeda, . Human activity recognition using temporal convolutional neural network architecture. Expert Systems with Applications, 191,2022.

N.S. Rani, P.N.Rao, P.Clinton,” Visual recognition and classification of videos using deep convolutional neural networks”, International Journal of Engineering & Technology, 7(2.31), pp.85-88,2018.

Y.L.Chang, T.H. Tan, W.H.Lee, L.Chang, Y.N. Chen, K.C. Fan, and M. Alkhaleefah, Consolidated Convolutional Neural Network for Hyper spectral Image Classification. Remote Sensing, 14(7), p.1571,2022

Z.Hu. Y.Zaho., M.Khushi,” . A survey of forex and stock price prediction using deep learning”, Applied System Innovation, 4(1), p.9,2021.

J.F. Pfahler, Exchange rate forecasting with advanced machine learning methods. Journal of Risk and Financial Management, 15(1), p.2,2022.

M.Z.Abedin, M.H.Moon,M.K..Hassan, P.Hajek,” Deep learning-based exchange rate prediction during the COVID-19 pandemic”, Annals of Operations Research, pp.1-52,2021.

I.C.Lee, C.H.Chang, F.N.Hwang,” Currency exchange rate prediction with long short-term memory networks based on attention and news sentiment analysis”, In 2019 International Conference on Technologies and Applications of Arti?cial Intelligence (TAAI) (pp. 1-6).2019, IEEE.

J.Chen et al.,”Exchange Rate Forecasting Based on Deep Learning and NSGA-II Models”, Computational Intelligence and Neuroscience, 2021.

Y.Zhang, S.Hamori,” The predictability of the exchange rate when combining machine learning and fundamental models”, Journal of Risk and Financial Management, 13(3), p.48,2020.

M.S.A. Sarkar and U.M.E. Ali,” EUR/USD Exchange Rate Prediction Using Machine Learning”, I. J. Mathematical Sciences and Computing, 1, 44-48, 2022.

S.Dash et.al,”A Novel Algorithmic Forex Trade and Trend Analysis Framework Based on Deep Predictive Coding Network Optimized with Reptile Search Algorithm”, Axioms, 11(8), p.396, 2022.

T.S. Madhulatha, M.A.S Ghori,” Foreign Exchange Rates Prediction for Time-series Data using Advanced Q-sensing Model”, 2022.

M.L.Shen et.al,” An effective hybrid approach for forecasting currency exchange rates”, Sustainability, 13(5), p.2761, 2021.

S.R.Das, M. Rout.,” A hybridized ELM-Jaya forecasting model for currency exchange prediction”, Journal of King Saud University – Computer and Information Sciences, vol.32, no.3, 2017.

J.Wang, X.Wang, J.Li, H.Wang,” A prediction model of CNN-TLSTM for USD/CNY exchange rate prediction”, Ieee Access, 9, pp.73346-73354, 2021.

K. Bataineh,” USD Exchange Rate Cycles Using Developed and Developing Currencies and Risk Factors”, Journal of Advances in Humanities Research, 1(1), pp.42-59,2022.

T.M.U.Ngan,” Forecasting foreign exchange rate by using ARIMA model: A case of VND/USD exchange rate. Methodology, 2014, p.2015”,2013.

F.Mansour, M.C.Yuksel, M.F.Akay,”Predicting Exchange Rate by Using Time Series Multilayer Perceptron”, 3rd International Mediterranean Science and Engineering Congress, IMSEC 2018, October 24-26, Adana/Turkey, 2018.

M.Karim,” The Forecast of Exchange Rates using Artificial Neural Networks, and their comparison to classic models”, UEL, Royal Duck Business School, 2014.

M.Savargiv, B. Masoumi, M.R.Keyvanpour,” A New Random Forest Algorithm Based on Learning Automata”, Hindawi, Computational Intelligence and Neuroscience, V. 2021, 2021.

X.Gao, J.Wen, C.Zhang,” An Improved Random Forest Algorithm for Predicting Employee Turnover”, Hindawi Mathematical Problems in Engineering, Volume 2019, ,2019 .

S. A. Zargar,” Introduction to sequence learning models: RNN,LSTM, GRU”, April,2021.

M.M.Panda, S.N.Panda, P.K.Pattnaik,”Exchange Multi currency exchange rate prediction using convolutional neural network”, Materials Today: Proceedings, 2021.